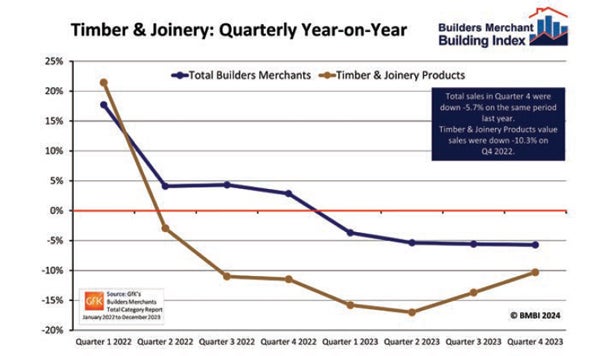

The latest figures from the Builders Merchants Building Index (BMBI), published in February, show that total value sales in Q4 2023 were -5.7% down compared to Q4 2022, with volumes falling -12% and prices rising +7.1%. With one more trading day in Q4 2023, like-for-like sales (which take the number of trading days into account) were -7.3% down.

Year-on-year, half of the 12 categories sold more in Q4 including work wear and safety wear (+8.6%) and decorating (+7.1%). However, the three largest categories all sold less: landscaping (-6.7%), heavy building materials (-7.3%) and timber and joinery products (-10.3%).

Quarter-on-quarter, total value sales for Q4 were down -15.7% compared to Q3. Volume sales fell-19.8% while prices rose +5.1%. With four fewer trading days in the most recent period, like-for-like sales were -10.1% lower.

Only two categories sold more. Timber and joinery products slumped -15.1%.

“As we look into the macroeconomic landscape, there’s a palpable sense of optimism brewing as the trajectory appears to be one of improvement for the future,” said Simon Woods, European sales, marketing and logistics director, West Fraser and BMBI’s expert for wood-based panels. “We witness lower inflation rates (from an uncomfortable high), a halting in the upward march of interest rates (again at a medium term high), and a stable unemployment environment.

These developments paint an improving picture, hinting at a strengthening economic foundation in the medium-term future.

“However, amidst these broader positive trends, the construction industry emerges as a curious anomaly, presenting a challenging market landscape. Despite the overarching macroeconomic improvements, the construction sector continues to grapple with its own set of complexities and hurdles.

“One notable aspect of the construction industry’s current predicament lies in the dynamics surrounding timber-related products. Importers face increasing costs, at least in the near term, as freight rates impact overall landed prices from a number of exporting regions.

“The crux of the issue lies in the soft demand prevalent within the construction market. Despite the broader economic landscape exhibiting future signs of recovery and stability, the construction industry contends with subdued levels of demand, casting a challenge over the prospects of timber-related products.

“In essence, while macroeconomic indicators hint at an overall improving picture, the construction industry serves as a stark reminder of the realities and challenges that persist in specific sectors of the economy.

The juxtaposition of lower inflation, stable unemployment, and the struggle within the construction market underscores the many-sided nature of economic dynamics, urging stakeholders to adopt a nuanced and adaptable approach in navigating the everevolving economic landscape.”